650 Credit Score: Is It Good Enough and How To Improve It?

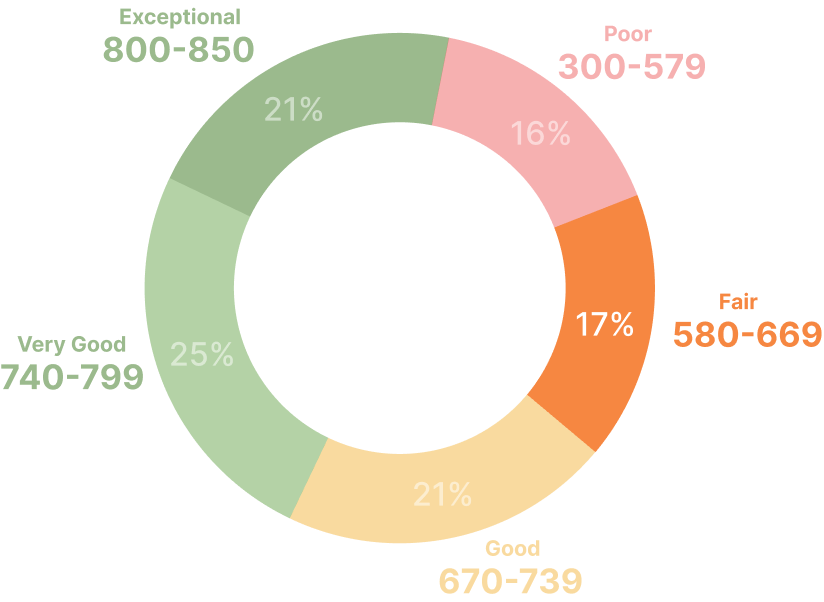

A 650 credit score falls under the fair category. It is considered ‘fairly okay,’ however, this score does not fall in the good range. The score may limit your access to the best interest rates and loan offers. Understanding its implications can make a world of difference in managing your financial well-being.

So, if you are wondering, “Is 650 a good credit score range?”

Read our blog to discover what it really entails.

| The median credit score for low-income Americans is 658. |

What Is a 650 Credit Score and Where Does It Stand?

As stated above, if your credit score is 650, you're in the fair credit range. All-in-all, it indicates that you've managed your credit responsibly, however, there may have been a few bumps along the way, like missed payments or carrying too much debt.

With this score, you can get access to credit, but lenders might perceive you as a bit of a risk. Therefore, loans and credit cards might still be available to you, though they could come with higher interest rates and lower credit limits.

Unlock a Better Credit Score with AI-Powered Credit Repair!

Try NowPercentage of Each Generation with 640-699 Credit Scores

| Gen Z | 22.5% |

| Millennials | 18.4% |

| Gen X | 18.3% |

| Baby Boomers | 15.0% |

Pros and Cons of a 650 Credit Score

Understanding its benefits and drawbacks is crucial, as they can significantly affect your financial opportunities. Let’s explore both sides to make informed decisions.

| Pros | Cons |

| Access to Credit: With a 650 credit score, you are likely to qualify for various types of credit, such as credit cards, personal loans, and auto loans. Regardless of the fact that you may not receive the best interest rates. | Limited Options: Individuals with a 650 credit score may not qualify for the most competitive interest rates or premium credit card offers. As a consequence, the terms and conditions offered to you may not be as favorable as they would be for those with higher scores. |

| Opportunity for Improvement: A 650 credit score provides room for growth. By making timely payments and managing your credit responsibly, you can work towards improving your score over time. | Higher Costs: Fair credit scores often come with higher interest rates, therefore, you could end up paying more in interest over the life of a loan compared to someone with an excellent credit score. |

| Financial Stability: Holding a 650 credit score indicates a level of financial responsibility and stability that can lead to better financial opportunities in the future. | Difficulty with Major Purchases: Securing large loans, such as mortgages or high-limit credit cards, may be challenging with a 650 credit score, limiting your borrowing options. |

Having covered the basics of a 650 credit score along with its benefits and drawbacks, let’s take a closer look at how this score can affect your financial landscape.

What Does a 650 Credit Score Help You Get?

| Type of Credit | Do You Qualify? |

| Credit Card | Yes |

| Home Loan | Yes |

| Auto Loan | Yes |

| Personal Loan | Maybe |

| 0% Intro APR Credit Card | No |

We've outlined answers to common questions below, helping you understand the possibilities a 650 score can offer.

Can I Get a Credit Card With a 650 Credit Score?

With this credit score, you can obtain a credit card, but your options may be more limited compared to individuals with higher credit scores.

Types of credit cards you may be eligible for:

▪ Secured Credit Cards

These cards require a cash deposit that serves as your credit limit and collateral, making them easier to get with a fair credit score. They can also help rebuild your credit.

▪ Subprime Credit Cards

These are designed for people with lower credit scores, though they often come with higher interest rates and fees.

▪ Standard Credit Cards

While you might qualify for standard credit cards, you may not be eligible for cards with premium rewards or low interest rates.

Can I Get a Car Loan with a 650 Credit Score?

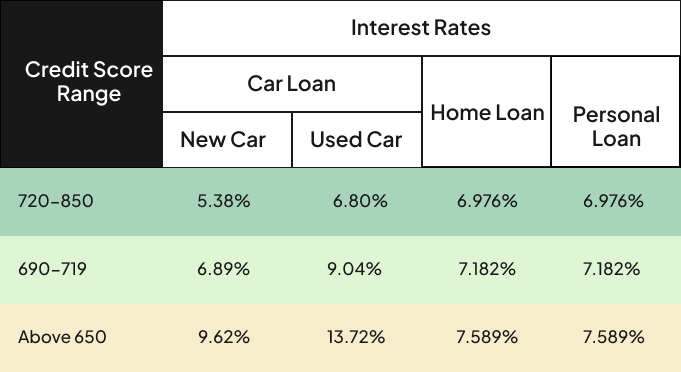

Having a credit score above 620 usually means you can qualify for a car loan with decent terms. A 650 score typically allows you to secure loans with a down payment and terms of 48 months or longer. Even though you have a fair score, lenders will assess other factors, such as your debt-to-income ratio, job history, credit background, and the car's value, before granting the loan.

The average interest rate for used and new cars for individuals with a fair credit score:

| Credit Score Category | Average Rate for Used Car | Average Rate for New Car |

| 601 to 650 | ±13% | ±9% |

Can I Get a Home Loan with a 650 Credit Score?

When buying a home, your credit score plays a crucial role. For instance, homebuyers with a credit score of 650 approximately secure a 7.45% interest rate on their mortgage.

However, many people ask, “What kind of home loan can I get with a 650 credit score?”

We have answered this question below:

✔ USDA Loan

Homebuyers looking to settle in a rural area might consider this loan. It offers competitive interest rates and requires no down payment. To qualify for a USDA loan, the property must be located in an eligible area, and the loan terms range up to 33 years, or 38 years for very low-income borrowers.

✔ Conventional Loan

Since conventional loans aren't government-insured, they often require a higher credit score. The monthly principal and interest payment won’t change for the life of the loan, so you get a consistent, predictable monthly payment.

✔ FHA Loan

FHA loans are accessible to those with low credit scores. Even with a credit score of 500, you can get an FHA loan by making a 10% down payment. These are conforming loans, which means there are limits on how much you can borrow, and these limits vary each year based on the area’s cost of living.

✔ VA Loan

Exclusively available to veterans, active military personnel, and their spouses, VA loans provide several advantages, including no down payment, lower interest rates, reduced closing costs, and the absence of private mortgage insurance.

Home Loan Interest Rates with a 650 Credit Score

We have considered the home loan price of $300,000, you can check the interest rates according to the home loan amount.

| Type of Loan | Interest Rates |

| USDA Loan | 4.875% |

| Conventional Loan | 5.500% |

| FHA Loan | 6.589% |

| VA Loan | 3.0% |

Can I Get a Personal Loan with a 650 Credit Score?

You can indeed obtain a personal loan with a 650 credit score, and loans are available even with scores lower than 650. While a score of 550 or higher is generally required, each lender has its own criteria. A 650 score increases your chances of approval, though the terms may not be the best.

Interest rates typically range from 13.48% to 19.65%. For better terms, consider bringing in a co-signer or joint borrower with a stronger credit profile and higher income.

Boost Your Credit with Ease!Download Our AI Credit Repair App Today for Fast, Automated Credit Improvements

Get StartedStrategies for Improving a 650 Credit Score

Effort invested wisely leads to rewarding results. That said, with some targeted effort, you can improve your score and enhance your access to better financial opportunities.

Here are some key things to consider if you want to improve your credit score:

- Pay bills on time

- Reduce credit card balances

- Check your credit report for errors

- Take help from a credit repair app

- Limit new credit applications

- Pay off existing debt

- Increase your credit limits

- Maintain a mix of credit types

- Keep old credit accounts open

- Consider a secured credit card

- Be patient and consistent

Boosting your credit score above 650 opens the door to better interest rates on a variety of loans. Check out the table below to see how much you can save!

Conclusion

To sum up, a 650 credit score may not be perfect. However, it is a solid starting point that can provide access to credit and pave the way for financial growth. By recognizing what your credit score means, and leveraging its strengths, you can confidently navigate the credit landscape and move closer to achieving financial success.

Moreover, with a 650 score, there's plenty of room for growth, and CoolCredit can help you make it happen. This DIY credit repair app provides everything you need to boost your credit score, from AI-generated dispute letters and credit monitoring to progress tracking and educational tools. Additionally, you can choose from options like Free DIY credit repair or Expert Assistance.

Download the app now and get on the path to a stronger credit future!

FAQs

Q: Is a 650 Credit Score Good?

A: A 650 credit score is generally considered to be in the "fair" range, which means it’s not bad, but it’s also not excellent. While it may qualify you for certain loans, credit cards, and financial products, you might not receive the most favorable interest rates or terms. Lenders may view a 650 score as somewhat risky, so you could face higher costs over time compared to someone with a higher score. However, with responsible financial behavior—like paying bills on time, reducing debt, and avoiding new credit inquiries—you can improve your score and unlock better financial opportunities in the future.

Q: How Much of a Home Loan Can I Get with a 650 Credit Score?

A: The exact loan amount will depend on various factors, including your income, debt-to-income ratio, and the type of loan you're applying for. While you may not be eligible for the largest loan amounts or the best rates, improving your credit score through timely payments and reducing existing debt could enhance your borrowing power and secure better terms in the future.

Q: How Much Can I Borrow With a Credit Score Under 650?

A: In assessing your loan application, banks look beyond your credit score. They review your income and expenses to understand how much you can afford to repay. While your credit score impacts the interest rate you receive, the actual loan amount is largely determined by your financial stability and repayment potential.

Q: Do I Need Collateral For a Personal Loan With a Credit Score Under 650?

A: When applying for a personal loan with a credit score under 650, you may be required to provide collateral, especially if your credit history suggests higher risk to lenders. Collateral serves as security for the lender, assuring that they can recover their funds if you default on the loan. However, the need for collateral can vary depending on the lender, the type of loan, and other factors such as your income and overall financial situation.