What Is Credit? Breaking Down the Basics

Credit, credit scores, and credit reports are interconnected pillars of your financial journey. Whether securing a credit card or purchasing your dream home, having a firm grasp of these concepts is key. While some factors carry more weight than others, understanding the foundation—‘What is credit’—empowers you to make informed decisions for lasting financial success.

This blog discusses all things credit, so let’s explore the essentials!

Leverage AI to boost your credit score!

Try NowWhat Is Credit?

At its core, credit is a system that lets you borrow money now and pay it back over time, including interest and fees. This arrangement is primarily available when you want to purchase a product or service.

So, why does good credit matter? The answer is—it reflects your financial reputation. Simply put, a solid credit history signals to lenders that you’re a reliable borrower. Moreover, it increases your chances of loan approvals and ensures you get competitive interest rates.

Types of Credit

There are several types of credit, each serving a different purpose and affecting your financial health. Although, the major ones are:

▪ Revolving Credit

It provides a more flexible way to make payments. You can borrow and repay the money repeatedly. As you pay down your balance, your available credit is replenished, allowing you to continue borrowing, such as credit cards, gas station cards, and HELOCs (Home Equity Line of Credit).

▪ Installment Credit

This type of credit involves borrowing a specific amount of money and agreeing to repay it with fixed monthly payments over a set period (usually years). Examples include personal loans, mortgages, and car loans.

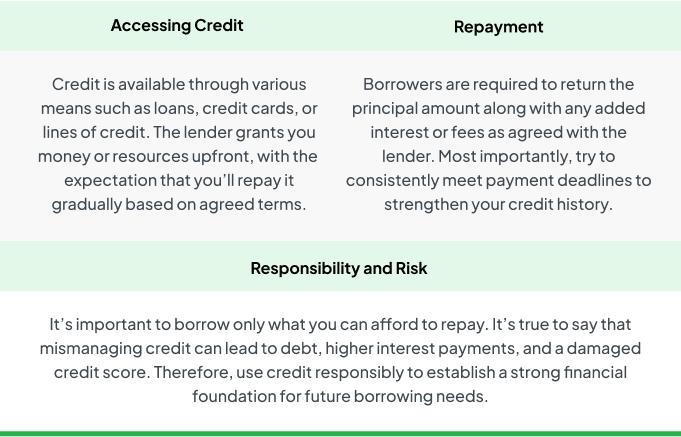

How Does Credit Work?

Again, credit is essentially an agreement between a borrower and a lender.

Here’s how it works:

Why You Need Credit?

You need credit for several reasons, as it is a vital aspect of managing your finances. The credit helps you in the following ways.

1. Purchasing Power: Credit enables you to afford significant purchases, like a home, car, or education. And you can break down the cost into manageable payments over time.

2. Building Financial History: Responsible use of credit helps build a good credit history. It is essential for demonstrating your ability to repay loans and manage financial obligations.

3. Emergencies: Having access to credit can provide a financial safety net, especially in situations when you might not have enough cash readily available.

4. Renting and Utility Services: Landlords and utility companies often check your credit to determine if you're financially reliable. A good credit history can help you secure a rental property and get favorable terms on utilities.

5. Financial Flexibility: It allows you to balance out payments and make purchases even when funds are temporarily tight. As a result, giving you more flexibility in managing your cash flow.

What Is Credit Score?

Ranging from 300 to 850, your credit score indicates your financial reliability. Lenders usually use it to assess your trustworthiness as a borrower. Additionally, it influences your loan approval, credit card limits, and interest rates. Two of the primary credit score models are FICO and VantageScore. They both consider similar factors when calculating your credit score. Nevertheless, they assign different importance to them, which means you’ll likely have a few different scores.

Credit scores naturally fluctuate, and small changes usually aren’t a big deal. However, if you see a drop of 10 points or more, you should review it. Since it could indicate missed payments or even something more serious, like identity theft.

How Are Credit Scores Calculated?

A good credit score is undeniably a key to unlocking better financial opportunities, but how is it determined? How can you tell if you’re on the right path to achieving a solid credit score? Let’s break it down by understanding the factors that influence it.

▪ Payment History

Your payment history accounts for the largest portion of your credit score. It shows whether you've paid your bills on time, including credit cards, loans, and other debts. However, late payments, defaults, or bankruptcies can have a significant negative impact on your score. In contrast, a history of on-time payments boosts your score.

▪ Credit Utilization

It refers to the amount of your available credit that you are currently using.

How to calculate your credit utilization ratio?

Total credit card balance/ Total credit card limit

Keeping this ratio under 30% signals to lenders that you manage your credit responsibly and can handle additional credit.

▪ Length of Credit History

The length of your credit history is often overlooked. In reality, it’s really important to calculate your credit score. A longer credit history shows lenders that you’ve had experience managing credit over time. Thus it leaves a positive impact on your score.

▪ Types of Credit

Successfully handling various credit types such as revolving credit and installment loans is a key factor in improving your credit scores.

▪ Recent Inquiries

Too many inquiries in a short period can lower your score slightly, as it could suggest financial instability. However, a single inquiry typically has a minimal impact and falls off your report after about two years.

Boost your credit intelligently. Let CoolCredit guide you with AI-driven insights.

Get StaredWhat Is Credit Report?

A credit report is a detailed record of an individual's credit history, including information about loans, credit cards, payment history, and current credit accounts. It is compiled by credit bureaus, such as Equifax, Experian, and TransUnion.

Lenders use credit reports to assess your creditworthiness when you apply for a loan or credit. The information in your credit report helps them decide whether to approve your application and what interest rate to offer.

What Information Appears on Credit Report?

✔Personal Information: Basic details like your name, address, social security number, and employment history.

✔Credit Accounts (Trade Lines): A record of all your credit accounts (e.g., credit cards, loans), including the current balance, payment history, and account status.

✔Payment History: Details of timely and late payments.

✔Credit Inquiries: Hard inquiries (lender-initiated credit checks) and soft inquiries (self-checks or pre-approvals).

✔Public Records: Bankruptcies, liens, or judgments.

✔Collections Accounts: Information on accounts that have been sent to collections due to non-payment. Your credit report essentially does not provide the credit score details. However, it provides the data that is used to calculate your credit score.

10 Tips on How To Build Your Credit

- Get a starter credit card – Use it wisely and pay on time to build a positive credit history.

- Always pay bills on time – Late payments can significantly hurt your credit score.

- Keep credit utilization low – Aim to stay below 30% of your credit limit to maintain a healthy score.

- Check credit reports regularly – Identify and fix errors that may harm your credit.

- Diversify credit types – A mix of credit cards and loans can improve your credit profile.

- Use credit repair apps – Track, monitor, and improve your credit score efficiently through applications.

- Avoid too many credit applications – Frequent hard inquiries can lower your score.

- Keep old accounts open – A longer credit history positively impacts your score.

- Use financing options smartly – Timely payments on financing plans help improve credit.

- Stay consistent – Building good credit takes time, discipline, and regular effort.

Conclusion

All things considered, knowing what is credit, and how credit scores and credit reports work is the first step toward financial freedom. This understanding empowers you to apply for loans, jobs, and housing with confidence. Strengthen your credit by making timely payments, managing credit utilization, diversifying your credit portfolio, and reviewing your credit reports regularly.

Meanwhile, if you find an error or want to improve your score? Let the CoolCredit app guide you on your journey to financial stability.

FAQs

Q: What Is Credit?

A: Credit is the ability to borrow money or access goods and services with the agreement to pay later, typically with interest.

Q: What Is a Credit Score?

A: Think of your credit score as a snapshot of your borrowing behavior, expressed in a number. It reflects your repayment habits, current credit usage, the length of your credit accounts, the types of credit, and any recent credit applications.

Q: What Is a Credit Report?

A: Your credit report is like a financial résumé, providing a detailed record of your credit history. It’s compiled by credit bureaus and reviewed by lenders to determine your trustworthiness in managing loans and repayments.

Q: What Is the Meaning of a Credit Information Report?

A: A Credit Information Report (CIR) is a detailed summary of an individual’s credit history, including loans, credit card usage, and payment behavior. It helps lenders assess creditworthiness and decide on loan approvals or credit limits.

Explore Similar Blogs

1. Types of Credit Explained: How Each One Impacts Your Score