How To Remove A Repossession From Your Credit Report?

Repossession is a derogatory mark that can stay on your credit record for a minimum of seven years. It strongly impacts credit ratings, causing a drop of 100 points or more, whether it’s a voluntary repossession or an involuntary one. The good news is that you can raise a dispute with credit authorities to take it down if it is inaccurate or false.

But it would be highly challenging to get it removed if it were due to some legit reason—perhaps you defaulted on a loan or had delinquent payments for several months in a row. This type of derogatory mark can hurt your scores enough that you’ll need to make significant efforts to rebuild your credit. So, in this blog, we’ll discuss all about repossession, its impact on your scores, and ways to remove it. We’ll also provide actionable tips to help rebuild your credit.

Speed up your credit repair with our advanced AI solutions.Fix your credit faster!

Start nowWhat Is Repossession and Its Impact on the Credit Scores

Repossession happens when the lender takes away an asset such as a vehicle, property, etc. (used as collateral) against some kind of secured loan. It can occur in two ways:

| Key Aspect | Involuntary Repossession | Voluntary Repossession |

| What Is It: | The lender seizes the collateral asset due to missed payments | The borrower willingly surrenders the asset, acknowledging their inability to pay |

| Process: | Professionals hired by the lender seize the asset | Borrower returns the asset directly to the lender |

| Outstanding Balance: | Borrower must pay the remaining balance, if any (in case the sale doesn't cover the outstanding amount) | Borrower still needs to pay the remaining balance if the sale doesn't cover the full cost |

| Impact on Credit Score: | Severe Impact; 50–150 score drop or more | Costs less than Involuntary Repossession; causes 50–150 score drop |

Why Do Repossessions Happen and How a Repossession Affects Your Credit?

It generally happens when you default on payments, single or multiple. Lenders may decide to repossess if they find you unable or unwilling to repay the loan. A repossession most often occurs with car loans, although it can be applicable to a range of assets, from furniture and appliances to just about any item assigned as collateral.

Causes of Repossession and How They Impact Your Credit Rating

| Cause | How It Leads to Repossession | Impact on Credit Scores | Estimated Score Drop |

| Late Payments | Failing to pay on time and repeated late payments signal financial instability, prompting repossession by the lender. | ▪ Significant negative impact ▪ Reduces creditworthiness | 60–110 points |

| Defaulting on Loan | When the borrower defaults on the loan, it may trigger repossession. Whether the lender acts after a single or multiple defaults depends on the contract terms. | ▪ Severe drop in credit score ▪ Stays on reports for up to 7 years | 100–150 points |

| Financial Troubles | Unexpected financial troubles resulting in difficulty in making timely payments lead to repossession after continued defaults. | ▪ Potential long-term damage to credit score ▪ Can stay on record for up to 7 years | 50–130 points |

| Credit Card Decline | Overexerting credit limits, the inability to prioritize timely payments, or having multiple credit cards but failing to maintain balance, increases the risk of defaulting, triggering repossession proceedings. | ▪ Negative impact on scores ▪ May cause a high credit utilization rate | 40–120 points |

| Health Issues | Medical emergencies or long-term medical expenses may affect income and financial stability, making you fall behind on payments—resulting in repossession. | ▪ Severely damages the credit score | 50–140 points |

| Poor Financial Planning | Failing to budget or allocate funds properly for loan repayments and poorly managed finances lead to missed payments and eventual default can prompt repossession. | ▪ Severely lowers the credit score ▪ Can stay on record for 7 years | 50–120 points |

Can Repossessions Be Removed From a Credit Report?

A repossession doesn’t stay longer than seven years on your credit report. So it gets automatically removed after the specified period. However, there are also other ways to get it removed depending on the cause of the repossession.

How to Get Repossession Off Your Credit Report?

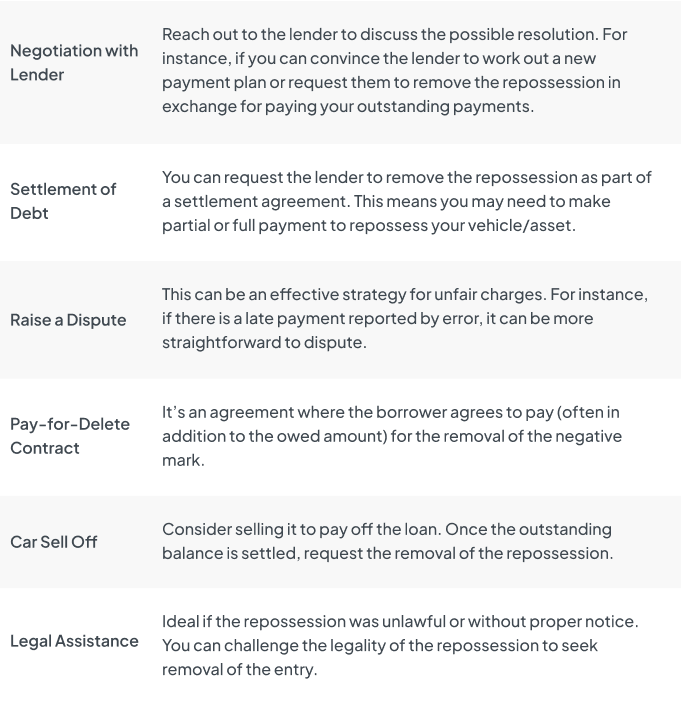

If the repossession was in error, you can simply raise a dispute and submit the evidence along with it to get it removed. This process takes 30-60 days.

For this, you can use the CoolCredit app to analyze your report and use its ready-to-use dispute letter templates without needing to draft one from scratch. There are also many other methods you can explore.

Methods for Removing a Repossession from Your Credit Report

However, if you are unable to get repossession off, its effect diminishes over time. In the meantime, you can improve your financial habits and make efforts to rebuild your credit.

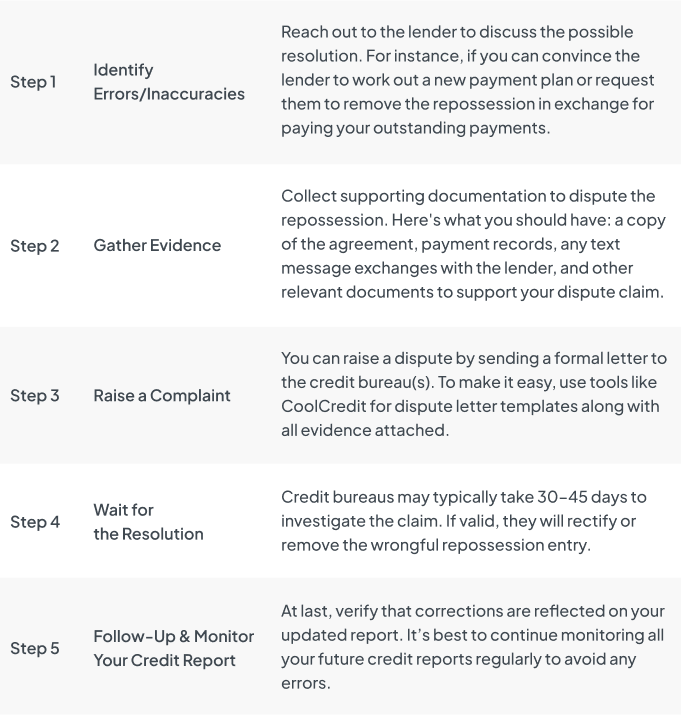

How Can I Dispute a Repossession on My Credit Report?

If there is an error, raise a dispute with the relevant credit bureau to have it cleared or get the derogatory mark removed for good.

You need to follow these 5 steps to raise a dispute:

Additional Steps Before Attempting to Remove Repossession

- Know Your Rights

Understand the repossession laws in your state or area. Knowing this can help you recognize any violations that may have happened, i.e., failure to provide proper notification or an illegal seizure.

- Check Statute of Limitations

It’s important to know that if a repossession occurred 7 years ago, it should automatically drop off your credit report. So, make sure to check the statute of limitation before pursuing the dispute that you are filing.

- Reach Out to the Lender

Before disputing, try convincing the lender to discuss possible solutions. You might offer a partial settlement or payment in full in exchange to remove repossession.

- Consult a Credit Expert (If Necessary)

If you may need to go through the legal route, seek advice from a credit repair professional for guidance tailored to your situation. They may assist with dispute filing & settlement negotiations.

How to Prevent a Repossession?

If you already know that due to some foreseen financial inadequacy you will be unable to make your payments on time, it’s best to reach out to the lender beforehand. This may give you a chance to negotiate a different payment plan that may fit your current situation.

Take the first step towards a higher credit score with AI credit repair app

Check your scoreHow Can I Improve My Credit After a Repossession?

By maintaining healthy financial habits, you can work on improving your credit score. Here are a few tips:

- Ensure making timely payments on all your debts without a single default.

- Maintain a low credit utilization rate, ideally, less than 30%.

- Try to make advance payments or pay more than the minimum payment in monthly installments whenever possible on your existing debt.

- It is best to clear your existing debt before obtaining a new one.

- Never apply for back-to-back loans, as frequent hard credit inquiries in a short time can make your score drop. Also, it can make your credit utilization high, which means you may get loans at high interest rates.

- You may consider getting a credit builder loan to repair your damaged credit rating.

- Use the CoolCredit app for regular credit monitoring and get suggestions on how to rebuild your credit.

Conclusion

Removing a repossession from a credit report is difficult, but it is not impossible. Actively disputing the errors, negotiating with the lender, or using apps such as CoolCredit, can help you move forward. If removal is impossible, remember that a repossession's effect diminishes over seven years. And with responsible financial planning, you can restore the damage to your scores.

Be proactive by assessing your reports regularly and addressing any mistakes immediately. As you continue to work on enhancing your financial standing and making wise financial moves, your score will begin to steadily improve.

FAQs

Q: What Is Repossession?

A: A repossession is the consequence of not making timely payments against a secured loan. The lender can seize the asset that was used as collateral.

Q: How Many Points Will I Lose with Repossession?

A: You can lose a minimum of 50 points to 100–150 points at most.

Q: How Long Does It Take to Rebuild Credit After Repossession?

A: For an unfair repossession, it takes around 30-60 days, provided you raise an objection and submit relevant evidence. Yet its rectification is long and torturous, probably taking a year or two or even more, or you may simply wait for seven years for the derogatory tick to fall off your credit report by itself.

Q: How Long Do Repossessions Stay on My Credit Report?

A: Repossession will remain on your report for a total of seven years from the delinquent date, i.e., the date of the origin of missed payments.

Q: How Do Voluntary Repossessions Affect My Credit?

A: You may still see your credit scores drop with voluntary repossession, but it may cost less than an involuntary repossession and also be less embarrassing. You may still lose 50-150 points.

Q: Can I Get a Loan After a Repossession?

A: Yes, you can, though due to the damage to your credit scores, you may get approved for loans at a very high interest rate until the repossession gets removed or the statute of limitation expires.

Q: Can I Get a Car Loan After a Repossession?

A: Yes, though it may be challenging. However, by working on rebuilding your credit score and getting a cosigner, it may be possible to get a car loan. Still, you may have to pay a higher interest rate if the repossession is still on your report.