How Long Do Collections Stay on Your Credit Report

A collection account can stay on your credit report for as long as seven years from the date of the first missed payment. Concerning, yes. But in the best case scenario, the impact of a collection account on your credit score may lessen over time. That is if you maintain good credit habits afterward.

For those still unsure what a collection account exactly is and those who want to know how to 'deal with it', this blog is a perfect read.

Unlock Your Credit Potential! Get Started with AI-Powered Credit Repair Now!

Improve CreditWhat Are Collections on Credit Reports?

Collections on credit reports are basically accounts that have gone unpaid and have been sent to a third-party collection agency. When you don’t pay a bill—like a credit card, medical bill, or even a utility bill—after a certain period (usually around 180 days), the original creditor gives up on collecting the debt and hands it off to a collection agency. And this doesn't exactly look good on your credit report.

This Is What Collections on Credit Report Can Look Like

| Type of Collection | What They Mean | Here Are Examples |

| Medical Collections | Unpaid medical bills that have been sent to collections after a certain period of non-payment. | Hospital bills, unpaid doctor visits, lab tests. |

| Credit Card Collections | Outstanding balances on credit cards that have not been paid and are turned over to collections. | Credit card debt that has remained unpaid for 180 days. |

| Utilities Collections | Unpaid utility bills (e.g., water, electricity, gas) sent to a collection agency after default. | Unpaid electricity bill, water service charges. |

| Student Loan Collections | Unpaid student loans that are in default and have been assigned to a collection agency. | Federal or private student loans in default. |

| Retail Collections | Unpaid accounts for retail store credit cards or financing agreements that have gone to collections. | Store credit cards (like Best Buy or Macy's) bills. |

| Auto Loan Collections | Unpaid auto loans that have been sent to a collections agency after defaulting on payments. | Car loans that have not been paid for several months. |

| Tax Collections | Unpaid taxes owed to the government that have been sent to collections, often leading to liens. | Unpaid federal or state taxes. |

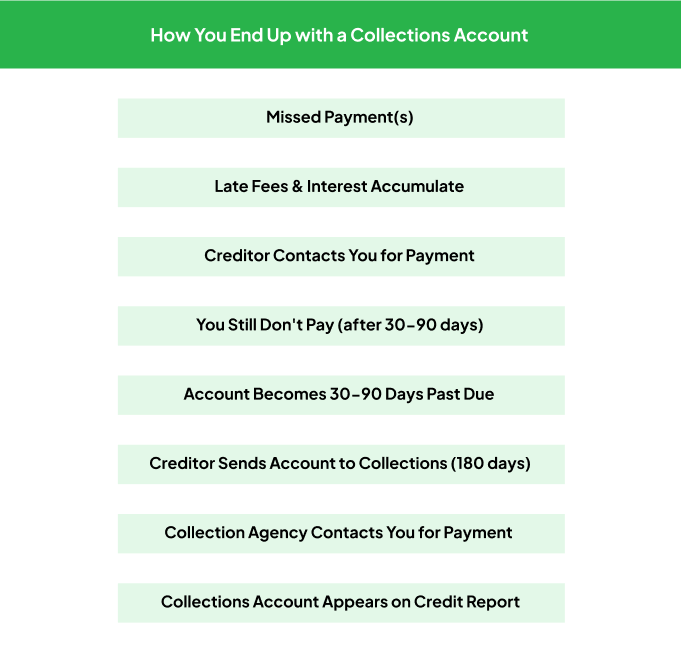

How Do You End up With a Collections Account on Your Credit Report?

Ending up with a collections account on your credit report can happen faster than you might think. It usually starts with a missed payment or two. Once you fall behind, your creditors will typically reach out, trying to get you back on track. If things go south and the debt remains unpaid for several months, they might decide to hand it off to a collection agency. That’s when the real trouble begins! Let’s break it down step by step with a flowchart to make it clearer.

How Long Does a Collection Stay on Your Credit History?

Like we covered earlier, the answer to ‘How long do collections stay on your credit report’ is up to seven years from the date of the original missed payment. That's a really long time. Moreover, collections are considered a derogatory remark on your credit report and a major red flag by lenders.

Because consider this: you had ample time to pay off the debt before it went to collections, but you couldn’t, which raises concerns for potential creditors in more than one way. And the repercussions? Dire.

(a) Collections on credit reports give 'an unreliable borrower', raising major concerns about your repayment ability.

(b) Assuming you even qualify for a loan - expect higher interest rates due to being viewed as risky.

(c) Limited credit options are a given.

(d) It can be really stressful, and finding the motivation to rebuild credit may not be easy to muster.

How Do Collections on Credit Report Affect Your Score?

Collections on your credit report can take a serious toll on your credit score. When a collection account appears, it signals to lenders that you’ve struggled to manage your debts, leading to a noticeable drop in your score. And now that you know the answer to ‘How long do collections stay on your credit report’, you should know that its impact is prolonged. Further, the exact impact depends on your overall credit history, but it’s common for collections to knock off a significant number of points, with its severity depending on various factors.

Let’s break down how collections affect your credit score:

| Factor | Effect of Collections |

| Credit Score | Collections can significantly lower your score. |

| Time Sensitivity | Recent collections hurt your score more than older ones. |

| Frequency | Multiple collections can lead to a larger score drop. |

| Severity of Debt | Higher unpaid debts in collections may impact your score more. |

| NOTE: The severity of the impact from a collection account can lessen over time, especially as it ages. While it may significantly lower your score initially, its influence diminishes as you demonstrate responsible credit behavior and as newer, positive accounts begin to balance out your credit history. |

Can You Remove Collections From Your Report Before Default Time?

Yes, you can get collections removed from your credit report before the seven-year mark, but it takes some effort and strategy. While it’s not a sure thing, you can try negotiating with the collection agency, disputing incorrect information, or asking for a goodwill deletion after you’ve settled the debt. Moreover, each scenario has its own process and results, so knowing your options can make a difference! Let’s go over the most common scenarios and your best bet to deal with them.

| Scenario | How to Remove | Chance of Success | Keep in Mind |

| Paid Collection (Goodwill Deletion) | Request a goodwill deletion from the creditor or agency after paying off the debt. | Moderate | Often works if you’ve had a good payment history before the collection. |

| Inaccurate Collection | Dispute inaccuracies with the credit bureaus. If the collection agency can’t verify it, the entry is removed. | High | Requires documentation proving errors. Always follow up. |

| Debt Settlement (Pay for Delete) | Negotiate with the collection agency to delete the account after payment. | Moderate | Ensure to get written confirmation before payment. |

| Statute of Limitations Passed | If the debt is past your state’s statute of limitations, you can dispute or negotiate. | Low to Moderate | Even if the debt is too old to sue, it can still appear on your report. |

| Identity Theft or Fraud | If a collection is due to identity theft, file a report and dispute the collection with evidence. | High | Providing proof of identity theft can lead to fast removal. |

| Debt Consolidation or Bankruptcy | After filing for bankruptcy, some collections may be removed, especially if discharged. | Low | Bankruptcy will affect your credit, but certain collections might be erased. |

| Settling with a Collection Agency | Negotiate a full or partial payment directly with the agency in exchange for removal. | Moderate | A "settled" status may still show up if deletion isn't negotiated. |

| Debt Validation | Request the collection agency to validate the debt within 30 days of notice. If they fail, it can be removed. | Moderate | You need to act quickly upon receiving the collection notice. |

How to Avoid Collections on Credit Report?

Avoiding collections on your credit report boils down to staying proactive with your debts. It’s all about managing payments before they get out of hand. Missing a payment here or there might seem like no big deal, but it can snowball quickly if you’re not careful. The key is to stay on top of your obligations and tackle any financial issues before they escalate.

Here’s what can save you the misery:

- Make It a Point to Pay Dues on Time: Set up reminders or automatic payments so you never miss a due date.

- Give Communicating With Creditors a Try: If you’re struggling, reach out to creditors before your account goes delinquent.

- Budgeting Is Everything: Regularly check your budget and adjust spending to ensure you can cover essentials.

- Set Aside Rainy Day Money: Having a safety net can help cover unexpected expenses without missing payments.

Smarter Credit Repair, Simplified for You!

Get StartedHow to Rebuild Credit After a Collection Account?

Rebuilding your credit after a collection account might feel overwhelming, but it’s totally doable with the right approach. Start by checking your credit report to understand where you stand and identify any negative marks. Then, focus on taking positive steps to raise your score over time.

Here are some effective strategies:

- Pay off any remaining debts to show you’re serious about improving your financial health.

- Set up a Booster Payment plan with CoolCredit to build a positive credit history.

- Open a secured credit card or become an authorized user on someone else's card to start building a positive payment history.

- Keep your credit utilization below 30% to maintain a healthy ratio.

- Regularly monitor your credit report to track progress and catch inaccuracies. You can do so through CoolCredit.

Conclusion

While collection accounts can be a significant hurdle, understanding how they work and taking proactive steps can help you manage their impact on your credit. By making timely payments and monitoring your credit, you can avoid future collections and start rebuilding your score. Remember, with dedication and the right strategies, restoring your credit is totally achievable.

FAQs

Q: How to Remove a Medical Collection Account?

A: Dispute any errors with the credit bureaus or strike a "pay-for-delete" deal with the collection agency. Recent credit reporting updates might also get paid medical debts wiped off.

Q: How Quickly Is Paid Off Debt Removed From a Credit Report?

A: Even after it's paid, debt can stick around for up to 7 years. But don’t worry—it’ll be marked as "paid" or "closed," which is way better for your credit.

Q: How to Improve Credit Score With Collections?

A: Pay or settle the collections, then dispute any incorrect details. Try for a goodwill deletion, or let time do its thing—collections drop off after 7 years.

Q: Can You Remove a Collection Account Without Paying?

A: Yep, if the collection is wrong, dispute it with the credit bureaus. If they can’t verify it, they’ve got to remove it.

Q: Do Collections Still Affect Your Credit After Being Paid?

A: Unfortunately, yes, but paying them off does help. The older they get, the less impact they have on your score.